Features

Valuing Trademarks in China: A Perspective on Common Methods

Published: June 16, 2021

Chris Fung Beijing Lifang & Partners Law Firm Beijing, China

Market Approach

When you buy or sell a house, the price is often determined by the price of similar properties. At auctions, the price is determined by what others are bidding.

The market approach is based on the prices that others have paid or would be willing to pay for an asset. The asset’s characteristics are not always considered, but external factors are. Because the asset being valued is not essential in this approach, some consider this to be a method of pricing rather than valuation.

This method depends on suitable comparators and market data. However, finding a suitable comparator might be trickier than one might imagine. For instance, under this approach, the brand above was valued at US $69 billion in 2019, while a competing brand was valued at US $11 billion. This represents a big difference in what might be perceived by some as similar brands and complicates comparison.

In bullish environments, the market approach leads to the overvaluation of assets, while in bearish situations, it leads to undervaluation. Moreover, such valuations include implicit presumptions that cannot be clearly expressed, such as public optimism or economic growth. Regardless of its weaknesses, this approach is easy to understand, making it popular in many situations.

According to the Guidelines, the market approach “is usually chosen for the purpose of capital contribution, transfer, licensed use or other transactions.” The author suggests that those seeking valuations always request a secondary method in addition to this one because markets can behave unpredictably.

Cash Flow Approach

The cash flow approach treats an asset’s value as equal to the value of all cash flows from that asset discounted to present values. This approach is less popular as it can be challenging and depends on the explicit assumptions of the evaluator. However, it is a rational model that considers inherent value based upon asset characteristics.

Discounting cash flows to present value raises issues that are best highlighted by a simple example:

In October 2000, the cost of rice was around US $6 per hundredweights (CWT). By 2020, that price had reached around US $12.

Perhaps many readers have noticed during their lives that the cost of things increases and that the buying power of money often decreases. This phenomenon also affects the value of trademarks. A comprehensive trademark valuation should consider this by discounting the value of future cash flows, which should at least equal the cost of capital.

During cash flow‒based valuations, we should also consider how a trademark will generate future cash flow. This can be difficult and subject to assumptions, such as inflation, revenue growth, royalty rates, changes in brand premium generated by a trademark, the renewal and continued existence of the trademark, and the trademark owner being rational.

Unfortunately, predictions are less accurate the further into the future they go. After all, 10 years ago, who could have predicted what 2020 would be like? Consider the brands that have risen or fallen in value over the last decade.

The Guidelines recognize this problem, noting that “the reasonableness of the future earnings forecast shall be comprehensively judged by considering the factors such as the reasonable production scale, market share, technical and management level of the appraisal target.”

Accordingly, because it is difficult to predict the future, predictions should be based on the risk profile of the person relying on the valuation. A 10-year outlook is the general practice. Predictions can go further into the future for those who are risk-loving than for those who are risk averse. Suitable assumptions must be considered on a case-by-case basis. As a rule of thumb, stable businesses have more distant prediction horizons, while volatile businesses should have shorter ones.

To put things in perspective, consider the following example:

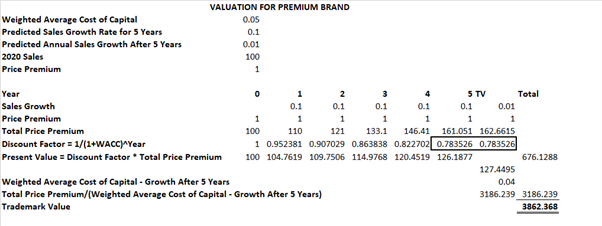

Premium Brand sells for 1 more than Generic Brand. Premium Brand has a brand premium of 1. Sales of Premium Brand were 100 in 2020. Analysts predict sales will increase by 10 percent per year for the next 5 years. We will assume that, after 5 years, growth slows to 1 percent. For simplicity, it is assumed that there is no cost in maintaining Premium Brand. The weighted average cost of capital of 5 percent shall be our discounting factor.

Using the discounted cash flow method, as shown below, the Premium Brand trademarks are worth 3,862.37.

The weighted average cost of capital (WACC) refers to the weighted average cost of debt, often in the form of interest paid, plus the cost of capital, which is the rate of return expected by investors.

The following is used to calculate WACC:

WACC= Cost of Equity×Percent of Equity + Cost of Debt×Percent of Debt

Growth figures often come from sales forecasts produced by marketing teams. Therefore, one might wish to adjust for the natural optimism that a marketing team might have, perhaps with the assistance of the organization’s finance team.

Note that this valuation method uses explicit assumptions, such as growth, WACC, and other things. These explicit assumptions can have an impact on negotiations and lead to disagreements over details.